Definition

Related Definitions

super fund

What is a super fund?

The super funds allow employees to save up till their retirement. Super funds are a pension programme that employees of a company can avail. The employee can either chose their super funds or can adopt the employer’s fund.

What is a MySuper account?

When an individual has super funds, then they own an account termed as MySuper account. It is a default account in which the employer will deposit all the super funds of the employees unless the employees opt for a different option. A MySuper account usually has lower fees and holders do not require to pay for extra features because of the simplicity in the present features.

Summary

- Super funds are pension funds that enable employees to save up till the time of retirement.

- Super funds can be of two types, accumulation funds ad defines benefit funds.

- Life cover, TPD insurance and income protection insurance can be availed under super funds.

Frequently Asked Questions (FAQs)

What are the types of super funds?

Super funds are of two types only, namely, accumulation funds and the defined benefits funds. Generally, the accumulation fund is the common super fund:

Accumulation funds – As the name suggests, the funds in the accumulation funds are accumulated over time, that is, they grow over time. The value of the super funds is dependent upon the amount contributed and the investment return. The contribution by employees and employers are known as a super contribution.

Defined benefits funds – The retirement benefits are calculated in the defined benefits funds rather than the investment returns. Public or corporate sector funds are the most common. Defined benefits funds are generally calculated by considering the following factors –

- The funds contributed by both employee and employer.

- The average salary before the retirement date.

- The years an employee worked with the employer.

Source: Copyright © 2021 Kalkine Media

What are the categories of super funds?

The super funds mainly fall into three categories, namely, corporate, industry, corporate and retail.

Retail super funds – These funds are run by investment companies and banking institutions. Anyone can opt for these funds. These funds provide a range of investment options. They are recommended by financial advisors and even act as an alternative to the MySuper account. The owner of these funds aims to make profits.

Industry super funds – Industry funds are of two types bigger and smaller. The bigger industry funds can be joined by anyone; however, smaller industry funds can only be utilized by specific industries like healthcare. Industry funds are the accumulation funds that offer MySuper account. Profit making is not the purpose of industry funds.

Public sector funds – It is for the government employees and the contribution of the employer is a minimum of 9.5%. These funds have low fees and offer a MySuper account. Profit-making is not the sole purpose of the public sector funds as the profit is put back in the funds.

Corporate super funds – It is arranged by the employers and it is operated by a board of trustees in large companies. It extends a wide range of investment alternatives, especially for those who manage large funds. The cost is low for larger employees and the cost is high for smaller employees. The profit is given to the members, unlike retail, where the portion of the profit is retained by the employer.

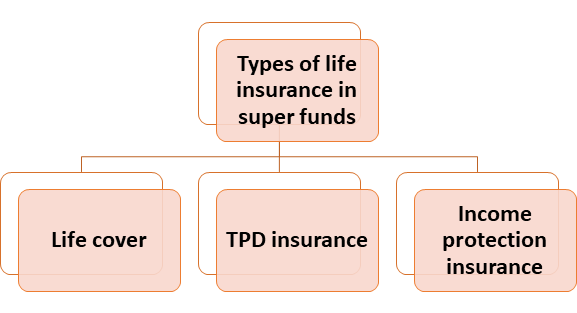

What are the types of life insurance that can be availed in super funds?

Three types of life insurances are offered by the super funds –

- Life cover: A lump sum amount is paid to the nominee in case the employee dies or get infected with a terminal illness. It is also known as death cover.

- TPD insurance: The benefit is paid to the employees if they become disabled or cannot work in the future.

- Income protection insurance: A regular income is paid to the employee in case they are not able to work with the organisation due to illness or some disability. The payment period can range from 2 to 5 years.

Source: Copyright © 2021 Kalkine Media

The majority of the super funds provides life and TPD insurance. Few super funds provide income protection. TPD insurance expires after the age of 65 and life insurance related benefits end at the age of 70.

When does insurance cancel in super funds?

The super fund’s accounts will cancel all the insurance-related benefits in case the accounts do not receive the contribution from either employee or employers for at least 16 months. Moreover, the super funds might cancel the insurance related benefits if the account balance is low. The super fund will communicate to the employee in case the cancellation process is underway.

Generally, the insurance facility is not extended to individuals who are below the age of 25, and in case the individual wants to have insurance, then the super fund members should be contacted with a reason to avail the insurance. The reason could be that the individual works in a dangerous job, for example, dealing with dangerous chemicals.

What are the advantages of insurance through super funds?

Low premium – The premium on the super funds’ insurance is generally low as the policies are bought in bulk.

Easy to pay – Since the premium amount is automatically deducted from the super balance, the premium paying process becomes easy.

Health check-up is limited – A default level of cover will be extended to the employee without undertaking health check-ups. This facility can be availed if the employee is not able to buy the insurance as they suffer from a serious health condition.

Increased cover – The cover amount can be leveraged from the default amount; however, it requires a medical check-up.

Tax-effective - The tax imposed on the contribution is generally lower than the marginal tax rate, therefore, it is tax effective.

What are the disadvantages of insurance through super funds?

Limited cover – The insurance coverage amount in the super funds is generally lower than the coverage of the insurance outside super funds. Moreover, the default insurance requires to fulfil some of the minimum eligibility requirements.

Cover can end – In case the super account has a low balance or inactive for a specified period of time, then the insurance can end. Then the employee will end up having no insurance.

Super balance is affected – Since the premium amounts are deducted from the super accounts, the savings for the retirement age reduces.