Definition

Related Definitions

Microfinance

What is microfinance?

Microfinance provides elementary financial services like credits, redeemable deposit accounts and asset insurances for people who have a lower income. Not all low-income group people get microfinance facilities; they need to be economically active people. For Example, self-employed, informal labourers, asset holders with no formal ownership titles and limited papers.

Since needs and borrowing capacity are limited, microfinance is mostly equated to providing small finances or mini-credits for small-entrepreneurs with lower socio-economic backgrounds.

Microfinance initially began with lending organisations offering micro-credit. They provided extremely tiny debts to borrowers who could offer collateral or had a stable source of income or any credit history. Microfinance now is also helpful in promoting economic progress, reducing joblessness, and boosting small industries. Some microfinance institutes nowadays even provide financial and business schooling to help their clients start small enterprise.

The objective is still the same, i.e., providing monetary help to impoverished people to ultimately become self-sustained.

Microfinance organisations can be various, ranging from commercial banks (exploring the low-end of the market), commercial microfinancing banks, nongovernmental organisations (NGOs), and cooperative banks. These organisations work to achieve profit, social impact, and environmental impact goals.

Highlights

- As the name suggests, microfinance is the provision of small loans to people belonging to socio-economically poor backgrounds.

- The finance is highly structured, and the aim is to make borrowers self-sufficient.

- It has been a successful tool for uplifting the weaker sections of society and for financial inclusion.

Frequently Asked Questions

How does microfinance work?

Copyright © 2021 Kalkine Media

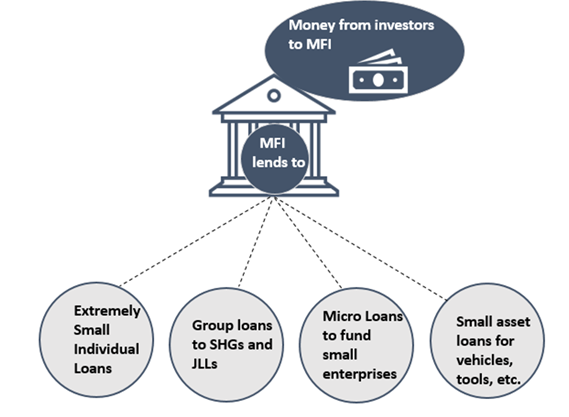

Borrowers can be individuals with some credit or collateral offering; if not, they can form groups and take collective loans from microfinance institutes.

The loans are minimal; their repayment schedule is long term, with small instalments favouring the borrower. The interest rate is usually low, sometimes waived off on regular repayment of instalments.

There is sometimes tied-up insurance of the loan to reduce the lending institutions risks. In addition, regular financial, educational training are organised for the borrowers. Also, lenders ensure that funds are utilised optimally.

In case of default of one member in a group loan, others become liable for repayment. If an Individual is borrowing, collateral is taken away. If the loan is for financing a minor asset or for enterprise capital and default in repayment, lenders can take away the asset or ask for ownership in the business.

It is highly regulated, and default risk is minimised; the aim is to make borrowers financially independent at the end of the loan.

Why does society need microfinance?

Not every person in society has access to financial markets. Low-income people have minimal credit and banking opportunities. Women are often thought out as not credit-worthy by lending organisations. No way to escape poverty as ‘poverty begets poverty.

Women are major microfinance debtors, holding 80% of loans in 2018 (data source: The 2019 Microfinance Barometer). Approximately 65% of the borrowers are from rural settings.

But microfinance provides structured access to funds to all such needy people to achieve- security, economic growth, and an opportunity to be self-sufficient.

Microfinance offers small business proprietors’ access to investment capital. Generally, it is very difficult for them to access credit or investment capital to grow their business. It provides finance and motivates borrowers to save money or get themselves insured. It can also serve as an important resource for those in the developing world.

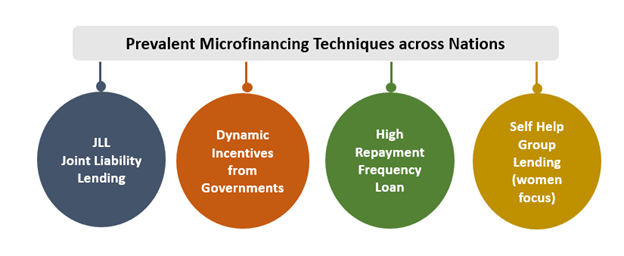

What are the prevalent microfinancing techniques?

Cost and risk are two essential considerations of any microfinancing institution. Though these two are difficult to achieve in poor socio-economic settings still microfinance is a successful concept. The success of micro-lending can be attributed to specific lending techniques adopted by them.

Copyright © 2021 Kalkine Media

By grouping borrowers into groups that share liability or essential characteristics like gender, micro financiers build trust. This way, a bond is created, working together to repay the loans, and become self-sufficient.

Microlending also takes place in incentives passed on by governments like interest waivers or high-frequency repayment schedules. The entire textile industry of Bangladesh stands up today on Microfinance.

What are the benefits of microfinance?

Source: © Neerazstockseller | Megapixl.com

- Microfinance helps to uplift the socio-economically left out people.

- It is a method of financial inclusion.

- It helps small and rural industries survive and expand.

- Microfinance eliminates joblessness and makes people self-sufficient.

- Microfinance helps spread financial and economic awareness.

- It helps create or mend credit reporting practices in developing nations.

- New laws have been advocated for protecting the earlier exploited poor and now governs their financial activities.

- Microfinance extends direct capital for small community industries.

- It has indirectly supported indigenous products manufactured by the rural poor.

- There is a new financial resilience in developing nations.

What are the hitches of microfinance?

- There have been examples where micro-financers have taken advantage of debtors.

- Microfinance loans may include high-interest rates spread over a longer time span, which is not beneficial if the time value of money concept is applied.

- Not many borrowers of such loans realise the improvement in net income.

- Many debtors use the finance for consumption purposes, not solving the purpose of the loan.

- Microfinance institutions are often labelled as making extorting money from the poor.

- Many big financial corporations have established for-profit microfinance departments raising social concerns.

- Larger bankers charge higher interest rates, thus creating a debt trap for poor borrowers.