Definition

Related Definitions

Going Concern

What is Going Concern?

In accounting, Going Concern is a principle which states the assumption that every business will continue to work for the foreseeable future. According to the Going Concern concept, an entity will continue its business for an indefinite period.

Source: Copyright © 2021 Kalkine Media

Understanding Going Concern

Going Concern concept states the assumption that every entity will be in business for the foreseeable future because of this concept many revenues and expenses are deferred for foreseeable future. Going concern principle is used by accountants at the time of preparing financial reports. The company, who runs with the going concern concept, does not liquidate its assets or anything. The concept also helps in taking decision related to sales of asset, reduction of expenses, introducing new products etc.

Companies make their strategies and plans by assuming that their business will continue to work for foreseeable future and record their assets, liabilities, expenses, and revenue in the balance sheet. Management uses these records of assets for making strategies with the motive of growth and survival of the business.

According to this concept, there are some expenses which are recorded as differed. For instance, company will get the advantage of expenditure on advertisement for more than a year. Assume a company spends £12,000 on advertisement and will get benefit for next 4 years. Here £12,000/4 = £3,000 is treated as expenses in one accounting year and P/L account will be charged with £3000 for next 4 years.

Frequently Asked Questions (FAQs)

What are the assumptions of Going Concern concept?

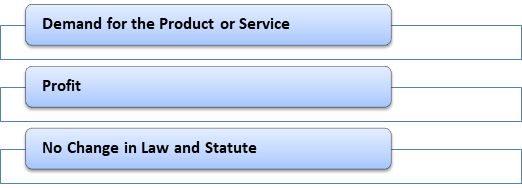

The term Going Concern is a principle that works with some assumptions. Every business runs with the assumption that it will continue in work endlessly. So, there are some factors which one must keep in mind to make the assumption work. These are:

Source: Copyright © 2021 Kalkine Media

Demand for the Product or Service: The company has to grow continuously by creating the demand of its product and services in the market and has focus on building the customer base by selling its product.

Profit: Profitability is in the priority to make work the concept of going concern. Profit is the blood of the life of business. The business always has to be in the state of profit in long term, even it faces loss in short term. The company has to grow every year.

No Change in Law and Statute: The company’s laws of administering and model should be rigid and positive in nature for the growth of business.

What are the advantages of Going Concern?

Advantages of going concern concept are:

- According to the Going Concern concept, there are some fixed assets that provide the benefits for many years. However, these assets are not treated as expenses in income statement and recorded in the balance sheet at cost throughout its life.

- This concept divides assets and liabilities as short and long term to smooth the functions of company in future. Short term includes less to up to 12 months and long term includes more than 12 months.

- This concept provides the basis on which revenue of a company is recorded over the related years.

- The assets and liabilities should be recorded at cost in the financial statements. It shows the security of the company and its long-term growth and expansion.

What are the disadvantages of Going Concern Concept?

Disadvantages of going concern concept are:

- A company’s financial statements are prepared at cost instead of current market value. If a company is in the situation of liquidation due to any unforeseen circumstance, the financial statements will treat with the current market value.

- Financial statements that are prepared on Going Concern concept at the time of wind up of business due to any reason represent the wrong information.

- Any change in the policies or laws of government that affect the concept of Going Concern of the business, and financial statements need to be prepared by following the concept of going concern and the laws again.

How red flag concept relates with going concern?

An auditor will issue a certificate by analysing and examining the financial statements of a company to know about the operating condition of the company to continuing in long term. Based on the financial reports of a company certain red flags may appear on the reports (financial statements) of publicly traded companies. These flags on financial statements indicates that the company is not in the state of a going concern in the future.

Normally, long-term assets are not presented in the quarterly statements of a company or in balance sheet. But if long-term assets appear in the quarterly statements, it indicated that the company is planning to sell these assets. It shows that the company is not able to meets its obligation without selling its assets that indicates the company is not in Going Concern concept.