Definition

Related Definitions

Due Diligence

What is due diligence?

The term due diligence found its origin in the 1930s relating to broker-dealers’ responsibilities towards investors. Under due diligence, the brokers were directed to conduct investigations on the securities being sold.

Due diligence is described as an investigation process conducted in various types of investment transactions. It is performed at different stages of the investment process across a wide variety of business situation.

Investment due diligence covers a variety of transactions and scenarios like M&A, debt financing, series funding for start-ups, long-term contracts. With several types of investment transaction, the process of due diligence could also vary depending on the transaction and scenario.

It is essentially an extensive investigation conducted by a potential investor seeking to invest in a business at a price obtained through negotiations or publicly-available source. The core investment due diligence does not include preliminary activities like identifying and filtering investment opportunities.

What is the purpose of due diligence?

The objective of due diligence is to review the initial assumptions of the investors on the investment opportunity. It is also conducted to identify risks and uncertainties that were not captured during the preliminary assessment.

An investor can come across additional nuances related to the investment opportunity during the due diligence process. As a result, this could lead to further negotiations with the business owner or even declining the investment opportunity.

With additional negotiations, terms and conditions of investment can change because of further information with the investors. Sometimes due diligence process may allow the investor to dictate the terms of the deal.

What are the types of due diligence?

Investment due diligence is carried across a range of transactions and can be tailored specifically for different investment situations and transactions. The type of transaction also impacts the considerations and objectives of the due diligence process.

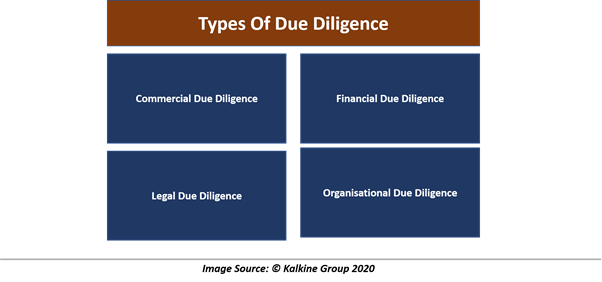

When a transaction is just limited to some asset sale, the investment due diligence process can be limited to an only assessment of the specific asset. Some basic due diligence includes:

Commercial due diligence

Commercial due diligence includes understanding the position of a business in the industry, including growth cycle, market share, prospects, clients. It is investigating resilience of profitability, scale and cost of the business.

Investors assess fundamentals of the company as well as industry, economy. An independent report by a consulting firm is used by investors, including companies. Investment expectations are evaluated compared to commercial prospects of business.

Financial due diligence

Financial due diligence seeks to test the viability of transaction financially. It includes modelling of future cash, revenues, costs etc. as well as analysing historical performance of the company over preceding years.

Investors assess cost base, assets, liabilities and other potential risks, which could result in outcomes like poor returns, lower profitability. Financial due diligence can be extended to tax liabilities and evaluation of tax benefits.

Legal due diligence

Legal due diligence is investigating all legal matters pertaining to the business, including litigation, ownership of assets, contingent liabilities, contractual obligations, incorporation, compliance. It also includes testing of intangible assets like patents, licenses.

Investors prefer to calculate the legal risk associated with a transaction, which could undermine the value of investments. Oftentimes outcomes of legal due diligence could give reasons to re-negotiate the deal.

Organisational due diligence

Organisational due diligence can include background checks of top-level management of the target company. Investors and management engage in the talks to discuss the viability of a business and potential outcomes over the future.

The organisational structure of the business is assessed, and assumptions are made. Employee agreements, contracts, remuneration are also investigated to ensure the business has assets like intellectual property.

What is Due diligence process?

Due diligence is usually performed in coordination across parties, including buyers, bankers, independent experts. Although there are no boundaries in the due diligence, basic due diligence goes like:

- Investor express intention to invest in the business or the business itself is asking investors for money led by top-level management.

- Both parties engage in talks regarding the transaction, opportunity, principal terms of investments, thus striking a relationship.

- A term sheet or letter of intent is prepared for the preliminary terms of transaction, including structure, price, process etc.

- After executing an initial agreement, they seek to conduct due diligence of the transaction and related matters.

- Investor and investee discuss the terms of accessing internal information regarding the business or target while conducting due diligence.

- Due diligence report is prepared after discussions with management, key people, plant visits, internal communication, and provided to the parties.

- An investor may present due diligence finding and look to negotiate the deal through changes in terms and conditions of the transaction.