Definition

Related Definitions

Demand

In economics, Demand is the buyer’s willingness and capacity to purchase a particular good or service by paying a suitable price. The price of a good or service depends on its market demand. If the demand for a good or service is more in the market and supply is less, the price of that good or service will jump and vice versa.

Understanding Demand:

Various companies worldwide spend a significant amount of money to determine the market demand before launching their business into a new region. Before the launch of a new product, a survey helps the supplier in gauging the demand for that good in the region. The survey also helps the company to evaluate how much money a consumer wants to pay for that service. Underestimation of demand may help the company fill its coffers, while an overestimation may lead to great losses.

The demand for a good or service is closely threaded to its supply. Suppliers want to offer their services and goods at higher prices to earn more profits, whereas consumers wish to grab the goods at lower prices. If the suppliers' prices are too high, the Demand for the product or service drops, disabling enough sales for the supplier. If the supplier offers very low prices, the Demand gets a shoot, but the supplier may not earn a substantial profit.

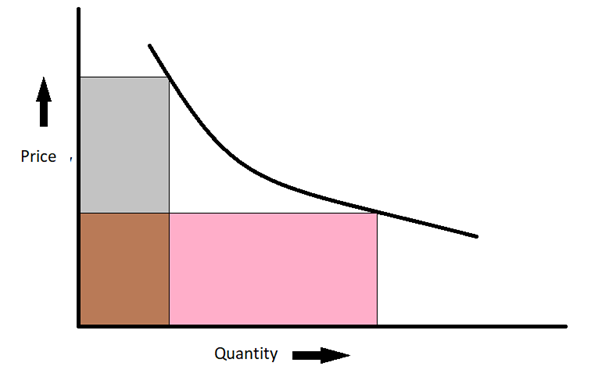

Demand Curve:

Source: Copyright © 2021 Kalkine Media Pty Ltd.

The Demand Curve is a graphical representation of a particular product or service's demand and supply relationship at a particular offered price. In a typical demand curve, the Y-axis represents the price of good or service, while the X-axis represents the quantity that people will buy at a specific price.

When the demand curve is relatively flat, the sales rise significantly even if there is a slight lowering in the prices offered by suppliers; however, when the demand curve is steep, a change in prices doesn't have a significant impact on the sales of a good or service.

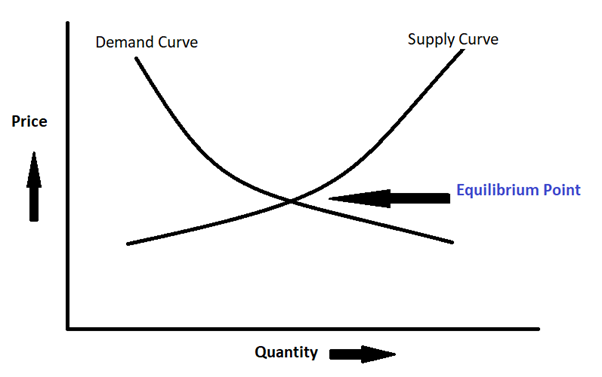

Market Equilibrium:

Market equilibrium is an ideal condition when the market demand counterbalances the market supply. The demand and supply curves intersect at a single point, which demarcates a situation when demand is equal to the supply.

Source: Copyright © 2021 Kalkine Media Pty Ltd.

Law of Supply and Demand:

The law of Demand and Supply is a theoretical explanation between the suppliers and buyers. The law governs the relationship between the offered price and consumers' willingness to buy a particular good or service. It is the most fundamental law in economics, which is followed in almost every business. The law helps to attain the market equilibrium by understanding consumers' willingness to set the prices of goods or services.

Aggregate Demand:

It is an economic measurement technique to determine the total demand for goods and services in an economy at a given price and under given tenure. It must not be confused with the Gross Domestic Product (GDP) which is the total amount of goods or services produced in an economy during a time frame. On the other hand, Aggregate Demand is the number of required goods or services in a specific price under a particular time frame. When the price of a good or service rises, it indicates that the aggregate supply is not adequate for business owners to expand their business and maintain the market equilibrium.